Ever wonder about gun control? Watch this video --- and pass it on.

Wisdom of Gun Control

2014-01-08

2013-12-22

How Obamacare Actually Works — Or Doesn't

The Hidden Impact of Obamacare and the Economy

By Jacqueline Leo4 hours ago

Obamacare has delivered another sucker punch to the middle class. This time it’s sticker shock.

Now that a few people can get past the tech problems of HealthCare.gov and actually see the real cost of insurance plans available, they are finding that Affordable Care is big hit to the family budget. And when the family budget gets hit in the solar plexus, guess what happens to consumer spending and the economy.

In California, policies for about 900,000 Californians are being canceled because of Obamacare’s mandates and about 2/3rd of these do not qualify for subsidies, according to The Chicago Tribune. The result—these folks will be paying higher premiums.

In Alabama, premiums have doubled for some middle class families like Courtney Long, a stay-at-home mother of four. She told WHNT News. “It’s devastating. I started crying,” said Long. “I mean, we have worked so hard to get out of credit card debt, get ahead on the car loan, transfer our mortgage to a 15 from a 30 year mortgage… and for what?”

In Tennessee, Sen. Lamar Alexander (R-TN) issued an analysis of a White House report and found the following:

— Today, a 27-year-old man in Memphis can buy a plan for as low as $41 a month. On the exchange, the lowest state average is $119 a month — a 190 percent increase.

— Today, a 27-year-old woman in Nashville can also buy a plan for as low as $58 a month. On the exchange, the lowest-priced plan in Nashville is $114 a month — a 97 percent increase. Even with a tax subsidy, that plan is $104 a month, almost twice what she could pay today.

— Today, women in Nashville can choose from 30 insurance plans that cost less than the administration says insurance plans on the exchange will cost, even with the new tax subsidy.

— In Nashville, 105 insurance plans offered today will not be available in the exchange.

In Washington State, Obamacare will increase the underlying cost of individually purchased health insurance by 34-80 percent on average, according to Forbes. The list goes on and on and includes Texas, Florida, New York, Illinois, Georgia and North Carolina. But premiums are just the beginning. The deductibles are outrageous, too.

A piece in Saturday’s The New York Times tells the story of Doug and Ginger Chapman, ages 55 and 54, a middle class couple “sitting on the health care cliff.” Their annual income of around $100,000 a year makes them ineligible for a subsidy in New Hampshire (if they earned under $94,000, it would cut their costs by half). They have to replace their family insurance which includes the two of them and their two sons. The premium cost alone, not including any deductible is $1,000 a month, or 12 percent of their income.

A piece in Saturday’s The New York Times tells the story of Doug and Ginger Chapman, ages 55 and 54, a middle class couple “sitting on the health care cliff.” Their annual income of around $100,000 a year makes them ineligible for a subsidy in New Hampshire (if they earned under $94,000, it would cut their costs by half). They have to replace their family insurance which includes the two of them and their two sons. The premium cost alone, not including any deductible is $1,000 a month, or 12 percent of their income.

The Times’ analysis found the following:

“The cost of premiums for people who just miss qualifying for subsidies rises rapidly for people in their 50s and 60s. In some places, prices can quickly approach 20 percent of a person’s income. Experts consider health insurance unaffordable once it exceeds 10 percent of annual income. By that measure, a 50-year-old making $50,000 a year, or just above the qualifying limit for assistance, would find the cheapest available plan to be unaffordable in more than 170 counties around the country, ranging from Anchorage to Jackson, Miss.”

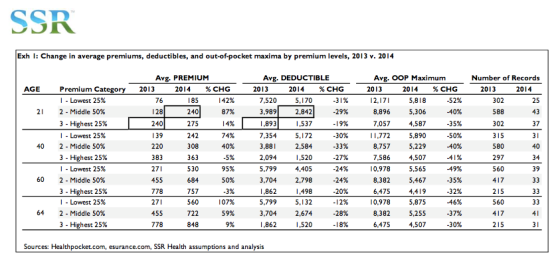

The other group that gets disproportionately hit is the young, according to Forbes. For a 40 year old, the 2013 average deductible was $4,045, and the cost increased 29 percent to $309. For a 64-year-old man, the cost of a plan with a $3,494 deductible increased 64 percent to $806.

The Real Impact of Obamacare is Yet to Come

If even a fraction of the middle class and upper middle income earners divert some of their discretionary dollars to pay for health care, it will have a significant impact on consumer spending. What will that mean for the economy? Consumer spending accounts for about 70 percent of the nation’s GDP, although experts say that number is likely to decline.

The top 20 percent of income earners account for about 40 percent of all spending in the U.S. When you increase the costs of health care and the new taxes associated with Obamacare, you can hear the wallets closing.

2013-12-21

Impeach Obama Now!

America is under attack from within. Over the last 4 ½ years, our nation has been transformed for the worse so much that one would hardly recognize it. We have a corrupt, Chicago politician in the White House who is bleeding our nation to death. Since he won re-election with the help of low information voters and a compliant media, the details of even further corruption has been revealed. The time has come and we must not relent until this happens.

IMPEACH OBAMA AND REMOVE HIM FROM OFFICE

Here’s why:

He has purposefully lied about the Benghazi atrocity, instructed others to lie, and intimidated whistleblowers who were guilty of nothing but a desire for justice and the truth. While our Libyan Ambassador burned and others were slaughtered, he went to bed, not even caring enough to make one phone call as to the status of the seven hours of Hell. Prior to the attacks, multiple requests for extra security in Benghazi, including from the murdered Ambassador Christopher Stevens, were refused by his regime. This was despite the fact that the British Embassy in Libya had been previously attacked just months earlier by Islamic terrorists. He has used taxpayer funds to run TV ads in Pakistan, pushing and promoting the lie that the Benghazi attacks were caused by a YouTube video.

At a time of the "Sequester" so-called cuts, equating to a insignificant cut in the "rate of growth" of government spending, he closed White House tours to our children, while sending hundreds of millions of taxpayer funds to the known terrorist group, The Muslim Brotherhood, in Egypt, including giving them F-16's and tanks.

He has treated our foreign friends like enemies and rewarded our enemies as if they were our friends.

He has inflicted the nation with over 20,000 pages of incoherent rules, regulations, and mandates in the form of ObamaCare, which, for the first time in history, gives the federal government the power to force its citizens to buy something that only the government approves of.

He has divided the country like in no time in history since the Civil War. He has pitted men against women, gay people against straight people, and used unAmerican, Marxist class warfare that has no place in a free America. He has caused racial strife by unjustifiably labeling anyone who disagrees with his USSR-style governance as a "racist."

He has degraded our people at every opportunity, apologizing for America on foreign soil. He has bowed to the Saudi Prince, humiliating our nation. To the Mexican people, he blamed the American people for his illegal gun-running operation "Fast and Furious." He apologized to the Mexican people for U.S. sovereignty while inferring that the lower region of our country still belonged to them.

He has continually and on numerous occasions abused the power of his office. To cover-up his regime's crimes in the Fast and Furious gun-running operation, in which the Obama regime gave guns to Mexican drug gangs, in an attempt to later attack the Second Amendment, he pleaded Executive Privilege.

He has exploded the already gargantuan national debt, increasing it by approximately 60% during his first term, while insisting that we must spend even more. He has failed to get even one of his budgets passed, even during the period when his own party held both houses of Congress, with his budget being defeated, 414-0, in the House and 99-0 in the Senate, without receiving even one vote from his own party.

He burned-up $862 billion on a "stimulus" plan that was supposed to create "shovel-ready jobs". Later, he admitted there was no such thing as a "shovel-ready" job.

He has promoted voter fraud at every possible occasion, and failed to convict proven voter intimidation based upon the skin color of the lawbreakers.

He has advertised and promoted America's food stamp program over Mexican airwaves to Mexican citizens, in an attempt to swarm our country with millions more in illegal aliens and further bankrupting our country with "Cloward and Piven" tactics.

He has sued several states repeatedly, stopping them from implementing the laws their citizens had approved, violating the Tenth Amendment in the process, while completely obliterating the constitutional principle of state sovereignty.

He has unconstitutionally bypassed Congress at every turn by using the federal bureaucracy to inflict massive and crushing laws on our people.

He has appointed dozens of unconstitutional "czars," unchecked by any balance of powers, who have served no purpose but to harass.

By all accounts he has created a Nixonian "Enemies List" which has included any individual, company, or industry that disagrees with his destructive policies. He has attacked and tried to silence our once "free press," even going to the extreme of instructing Americans which media sources they should listen to.

He embarrassed and harmed our relationship with our ally, Great Britain, by sending an official U.S. delegation to Socialist dictator, Hugo Chavez's funeral, but yet sending no one to the great defender of liberty, the great former British Prime Minister, Margaret Thatcher's funeral.

He has used tragedy and crisis to attack our constitutional freedoms, using the Sandy Hook shootings to infringe upon our non-negotiable Second Amendment rights. He used the Benghazi terrorist attacks, blaming them on the First Amendment which would allow a YouTube video critical of Islam.

He has unconstitutionally attacked our sacred freedom of religion, a God-given right guaranteed by our Founders in the First Amendment.

President Obama is the most corrupt president in U.S. history. His actions are against everything this country was founded upon and stands for. He is a danger to America. We are therefore calling for his impeachment and removal from office. We urge you to join us for the good of our nation and to keep the legacy of our Founding Fathers alive.

Can ObamaCare Possibly Be / Get Any Worse?

Story of the year

By Charles Krauthammer

The lie of the year, according to Politifact, is “If you like your health care plan, you can keep it.” But the story of the year is a nation waking up to just how radical Obamacare is — which is why it required such outright deception to get it passed in the first place.

Obamacare was sold as simply a refinement of the current system, retaining competition among independent insurers but making things more efficient, fair and generous. Free contraceptives for Sandra Fluke. Free mammograms and checkups for you and me. Free (or subsidized) insurance for some 30 million uninsured. And, mirabile dictu, not costing the government a dime.

In fact, Obamacare is a full-scale federal takeover. The keep-your-plan-if-you-like-your-plan ruse was a way of saying to the millions of Americans who had insurance and liked what they had: Don’t worry. You’ll be left unmolested. For you, everything goes on as before.

That was a fraud from the very beginning. The law was designed to throw people off their private plans and into government-run exchanges where they would be made to overpay — forced to purchase government-mandated services they don’t need — as a way to subsidize others. (That’s how you get to the ostensible free lunch.)

It wasn’t until the first cancellation notices went out in late 2013 that the deception began to be understood. And felt. Six million Americans with private insurance have just lost it. And that’s just the beginning. By the Department of Health and Human Services’ own estimates, about 75 million Americans would have plans that their employers would have the right to cancel. And millions of middle-class workers who will migrate to the exchanges and don’t qualify for government subsidies will see their premiums, deductibles and co-pays go up.

It gets worse. The dislocation extends to losing one’s doctor and drug coverage, as insurance companies narrow availability to compensate for the huge costs imposed on them by the extended coverage and “free” services the new law mandates.

But it’s not just individuals seeing their medical care turned upside down. The insurance providers, the backbone of the system, are being utterly transformed. They are rapidly becoming mere extensions of the federal government.

Look what happened just last week. Health and Human Services unilaterally and without warning changed coverage deadlines and guidelines. It asked insurers to start covering people on Jan. 1 even if they signed up as late as the day before and even if they hadn’t paid their premiums. And is “strongly encouraging” them to pay during the transition for doctor visits and medicines not covered in their current plans (if covered in the patient’s previous — canceled — plan).

On what authority does a Cabinet secretary tell private companies to pay for services not in their plans and cover people not on their rolls? Where in Obamacare’s 2,500 pages are such high-handed dictates authorized? Does anyone even ask? The bill itself is simply taken as a kind of blanket warrant for HHS to run, regulate and control the whole insurance system.

Remember the uproar over forcing religious institutions to provide contraception coverage? The president’s “fix” was a new regulation ordering insurers to provide these services for free. Apart from the fact that this transparent ruse does nothing to resolve the underlying issue of conscience — God sees — by what right does the government order private companies to provide free services for anyone?

Three years ago I predicted that Obamacare would turn insurers into the lapdog equivalent of utility companies. I undershot. They are being treated as wholly owned subsidiaries. Take the phrase “strongly encouraging.” Sweet persuasion? In reality, these are offers insurers can’t refuse. Disappoint your federal master and he has the power to kick you off the federal exchanges, where the health insurance business of the future is supposed to be conducted.

Moreover, if adverse selection drives insurers into a financial death spiral — too few healthy young people to offset more costly, sicker, older folks — their only recourse will be a government bailout. Do they really want to get on the wrong side of the White House, their only lifeline when facing insolvency?

I don’t care a whit for the insurance companies. They deserve what they get. They collaborated with the White House in concocting this scheme and are now being swallowed by it. But I do care about the citizenry and its access to a functioning, flourishing, choice-driven medical system.

Obamacare posed as a free-market alternative to a British-style single-payer system. Then, during congressional debate, the White House ostentatiously rejected the so-called “public option.” But that’s irrelevant. The whole damn thing is the public option. The federal government now runs the insurance market, dictating deadlines, procedures, rates, risk assessments and coverage requirements. It’s gotten so cocky it’s now telling insurers to cover the claims that, by law, they are not required to.

Welcome 2014, our first taste of nationalized health care.

2013-12-17

More Astonishing Government Waste! It Never Ends!

Is it possible that government waste of our tax dollars could be more egregious? Read it and weep!

U.S. Federal Government WASTE - 2013

Sad!

U.S. Federal Government WASTE - 2013

Sad!

2013-12-10

What Do You Know About Benghazi?

Can you answer these questions about Benghazi? If not, why not?

(click on the following link)

Benghazi Questions You Should Be Able To Answer

(click on the following link)

Benghazi Questions You Should Be Able To Answer

How and Why the Government Caused the 2008 Financial Crisis

FOREWORD: The 2008 financial crisis cost the U.S. economy more than $22 trillion according to the U.S. Government Accountability Office.

The case for repealing Dodd-Frank

PETER J. WALLISON holds the Arthur F. Burns Chair in Financial Policy Studies at the American Enterprise Institute. Previously he practiced banking, corporate, and financial law at Gibson, Dunn & Crutcher in Washington, D.C., and in New York. He also served as White House Counsel in the Reagan Administration. A graduate of Harvard College, Mr. Wallison received his law degree from Harvard Law School and is a regular contributor to the Wall Street Journal, among many other publications. He is the editor, co-editor, author, or co-author of numerous books, including Ronald Reagan: The Power of Conviction and the Success of His Presidency and Bad History, Worse Policy: How a False Narrative about the Financial Crisis Led to the Dodd-Frank Act.

The following is adapted from a speech delivered at Hillsdale College on November 5, 2013, during a conference entitled “Dodd-Frank: A Law Like No Other,” co-sponsored by the Center for Constructive Alternatives and the Ludwig Von Mises Lecture Series.

The 2008 financial crisis was a major event, equivalent in its initial scope—if not its duration—to the Great Depression of the 1930s. At the time, many commentators said that we were witnessing a crisis of capitalism, proof that the free market system was inherently unstable. Government officials who participated in efforts to mitigate its effects claim that their actions prevented a complete meltdown of the world’s financial system, an idea that has found acceptance among academic and other observers, particularly the media. These views culminated in the enactment of the Dodd-Frank Act that is founded on the notion that the financial system is inherently unstable and must be controlled by government regulation.

We will never know, of course, what would have happened if these emergency actions had not been taken, but it is possible to gain an understanding of why they were considered necessary—that is, the causes of the crisis.

Why is it important at this point to examine the causes of the crisis? After all, it was five years ago, and Congress and financial regulators have acted, or are acting, to prevent a recurrence. Even if we can’t pinpoint the exact cause of the crisis, some will argue that the new regulations now being put in place under Dodd-Frank will make a repetition unlikely. Perhaps. But these new regulations have almost certainly slowed economic growth and the recovery from the post-crisis recession, and they will continue to do so in the future. If regulations this pervasive were really necessary to prevent a recurrence of the financial crisis, then we might be facing a legitimate trade-off in which we are obliged to sacrifice economic freedom and growth for the sake of financial stability. But if the crisis did not stem from a lack of regulation, we have needlessly restricted what most Americans want for themselves and their children.

The Federal Housing Administration, or FHA, established in 1934, was authorized to insure mortgages up to 100 percent, but it required a 20 percent down payment and operated with very few delinquencies for 25 years. However, in the serious recession of 1957, Congress loosened these standards to stimulate the growth of housing, moving down payments to three percent between 1957 and 1961.

Predictably, this resulted in a boom in FHA insured mortgages and a bust in the late '60s. The pattern keeps recurring, and no one seems to remember the earlier mistakes. We loosen mortgage standards, there’s a bubble, and then there’s a crash. Other than the taxpayers, who have to cover the government’s losses, most of the people who are hurt are those who bought in the bubble years, and found—when the bubble deflated—that they couldn’t afford their homes.

Congress planted the seeds of the crisis in 1992, with the enactment of what were called “affordable housing” goals for Fannie Mae and Freddie Mac. Before 1992, these two firms dominated the housing finance market, especially after the federal savings and loan industry—another government mistake—had collapsed in the late 1980s. Fannie and Freddie’s role, as initially envisioned and as it developed until 1992, was to conduct what were called secondary market operations, to create a liquid market in mortgages. They were prohibited from making loans themselves, but they were authorized to buy mortgages from banks and other lenders. Their purchases provided cash for lenders and thus encouraged home ownership by making more funds available for more mortgages. Although Fannie and Freddie were shareholder-owned, they were chartered by Congress and granted numerous government privileges. For example, they were exempt from state and local taxes and from SEC regulations. The president appointed a minority of the members of their boards of directors, and they had a $2.25 billion line of credit at the Treasury. As a result, market participants believed that Fannie and Freddie were government-backed, and would be rescued by the government if they ever encountered financial difficulties.

This widely assumed government support enabled these GSEs to borrow at rates only slightly higher than the U.S. Treasury itself, and with these low-cost funds they were able to drive all competition out of the secondary mortgage market for middle-class mortgages—about 70 percent of the $11 trillion housing finance market. Between 1991 and 2003, Fannie and Freddie’s market share increased from 28 to 46 percent. From this dominant position, they were able to set the underwriting standards for the market as a whole; few mortgage lenders would make middle-class mortgages that could not be sold to Fannie or Freddie.

Over time, these two GSEs had learned from experience what underwriting standards kept delinquencies and defaults low. These required down payments of 10 to 20 percent, good credit histories for borrowers, and low debt-to-income ratios after the mortgage was closed. These were the foundational elements of what was called a prime loan or a traditional mortgage, and they contributed to a stable mortgage market through the 1970s and most of the 1980s, with mortgage defaults generally under one percent in normal times and only slightly higher in rough economic waters. Despite these strict credit standards, the homeownership rate in the United States remained relatively high, hovering around 64 percent for the 30 years between 1964 and 1994.

In a sense, government backing of the GSEs and their market domination was their undoing. Community activists had kept the two firms in their sights for many years, arguing that Fannie and Freddie’s underwriting standards were so tight that they were keeping many low- and moderate-income families from buying homes. The fact that the GSEs had government support gave Congress a basis for intervention, and in 1992 Congress directed the GSEs to meet a quota of loans to low- and middle-income borrowers when they acquired mortgages. The initial quota was 30 percent: In any year, at least 30 percent of the loans Fannie and Freddie acquired must have been made to low- and moderate-income borrowers—defined as borrowers at or below the median income level in their communities. Although 30 percent was not a difficult goal, the Department of Housing and Urban Development (HUD) was given authority to increase the goals, and Congress cleared the way for far more ambitious requirements by suggesting in the legislation that down payments could be reduced below five percent without seriously impairing mortgage quality. In succeeding years, HUD raised the goal, with many intermediate steps, to 42 percent in 1996, 50 percent in 2000, and 56 percent in 2008.

In order to meet these ever-increasing goals, Fannie and Freddie had to reduce their underwriting standards. In fact that was explicitly HUD’s purpose, as many statements by the department at the time made clear. As early as 1995, the GSEs were buying mortgages with three percent down payments, and by 2000 Fannie and Freddie were accepting loans with zero down payments. At the same time, they were also compromising other underwriting standards, such as borrower credit standards, in order to find the subprime and other non-traditional mortgages they needed to meet the affordable housing goals.

These new easy credit terms spread far beyond the low-income borrowers that the loosened standards were intended to help. Mortgage lending is a competitive business; once Fannie and Freddie started to reduce their underwriting standards, many borrowers who could have afforded prime mortgages sought the easier terms now available so they could buy larger homes with smaller down payments.

Thus, home buyers above the median income were gaining leverage through lower down payments, and loans to them were decreasing in quality. In many cases, these homeowners were withdrawing cash from the equity in their homes through cash-out refinancing as home prices went up and interest rates declined in the mid-2000s. By 2007, 37 percent of loans with down payments of three percent went to borrowers with incomes above the median.

As a result of the gradual deterioration in loan quality over the preceding 16 years, by 2008, just before the crisis, 56 percent of all mortgages in the U.S.—32 million loans—were subprime or otherwise low quality. Of this 32 million, 76 percent were on the books of government agencies or institutions like the GSEs that were controlled by government policies. This shows incontrovertibly where the demand for these mortgages originated.

With all the new buyers entering the market because of the affordable housing goals, housing prices began to rise. By 2000, the developing bubble was already larger than any bubble in U.S. history, and it kept growing until 2007, when—at nine times the size of any previous bubble—it finally topped out and housing prices began to fall.

Housing bubbles tend to suppress delinquencies and defaults while the bubble is growing. This happens because as prices rise, it becomes possible for borrowers who are having difficulty meeting their mortgage obligations to refinance or sell the home for more than the principal amount of the mortgage. In these conditions, potential investors in mortgages or in mortgage-backed securities receive a strong affirmative signal; they see high-yielding mortgages—loans that reflect the riskiness of lending to a borrower with a weak credit history—but the expected delinquencies and defaults have not occurred. They come to think, “This time it’s different”—that the risks of investing in subprime or other weak mortgages are not as great as they’d thought. Housing bubbles are also pro-cyclical. When they are growing, they feed on themselves, as buyers bid up prices so they won’t lose a home they want. Appraisals, based on comparable homes, keep pace with rising prices. And loans keep pace with appraisals, until home prices get so high that buyers can’t afford them no matter how lenient the terms of the mortgage. But when bubbles begin to deflate, the process reverses. It then becomes impossible to refinance or sell a home when the mortgage is larger than the home’s appraised value. Financial losses cause creditors to pull back and tighten lending standards, recessions frequently occur, and would-be purchasers can’t get financing. Sadly, many are likely to have lost their jobs in the recession while being unable to move where jobs are more plentiful, because they couldn’t sell their homes without paying off the mortgage balances. In these circumstances, many homeowners are tempted to walk away from the mortgage, knowing that in most states the lender has recourse only to the home itself.

With the largest housing bubble in history deflating in 2007, and more than half of all mortgages made to borrowers who had weak credit or little equity in their homes, the number of delinquencies and defaults in 2008 was unprecedented.

One immediate effect was the collapse of the market for mortgage-backed securities that were issued by banks, investment banks, and subprime lenders, and held by banks, financial institutions, and other investors around the world.

These were known as private label securities or private mortgage-backed securities, to distinguish them from mortgage-backed securities issued by Fannie and Freddie. Investors, shocked by the sheer number of mortgage defaults that seemed to be underway, fled the market for private label securities; there were now no buyers, causing a sharp drop in market values for these securities.

This had a disastrous effect on financial institutions. Since 1994, they had been required to use what was called “fair value accounting” in setting the balance sheet value of their assets and liabilities. The most significant element of fair value accounting was the requirement that assets and liabilities be marked-to-market, meaning that the balance sheet value of assets and liabilities was to reflect their current market value instead of their amortized cost or other valuation methods.

Marking-to-market worked effectively as long as there was a market for the assets in question, but it was destructive when the market collapsed in 2007. With buyers pulling away, there were only distress-level prices for private mortgage-backed securities. Although there were alternative ways for assets to be valued in the absence of market prices, auditors—worried about their potential liability if they permitted their clients to overstate assets in the midst of the financial crisis—would not allow the use of these alternatives. Accordingly, financial firms were compelled to write down significant portions of their private mortgage-backed securities assets and take losses that substantially reduced their capital positions and created worrisome declines in earnings. When Lehman Brothers, a major investment bank, declared bankruptcy, a full-scale panic ensued in which financial institutions started to hoard cash. They wouldn’t lend to one another, even overnight, for fear that they would not have immediate cash available when panicky investors or depositors came for it. This radical withdrawal of liquidity from the market was the financial crisis.

The Affordable Care Act, better known as ObamaCare, has received all the attention as the worst expression of the Obama presidency, but Dodd-Frank deserves a look. Just as ObamaCare was the wrong prescription for health care, Dodd-Frank was based on a faulty diagnosis of the financial crisis. Until that diagnosis is corrected—until it is made clear to the American people that the financial crisis was caused by the government rather than by deregulation or insufficient regulation—economic growth will be impeded. It follows that when the true causes of the financial crisis have been made clear, it will become possible to repeal Dodd-Frank.

This has happened before. During the 1930s, the dominant view was that the Depression was caused by excessive competition. It seems crackpot now, but the New Dealers thought that too much competition drove down prices, caused firms to fail, and thus increased unemployment. The Dodd-Frank of the time was the National Industrial Recovery Act. Although it was eventually overturned by the Supreme Court, its purpose was to cartelize industry and limit competition so that businesses could raise their prices. It was only in the 1960s, when Milton Friedman and Anna Schwartz showed that the Depression was caused by the Federal Reserve’s monetary policy, that national policies began to move away from regulation and toward competition. What followed was a flood of deregulation—of trucking, air travel, securities, and communications, among others—which has given us the Internet, affordable air travel for families instead of just business, securities transactions at a penny a share, and Fedex. Ironically, however, the regulation of banking increased, accounting for the problems of the industry today.

If the American people come to recognize that the financial crisis was caused by the housing policies of their own government—rather than insufficient regulation or the inherent instability of the U.S. financial system—Dodd-Frank will be seen as an illegitimate response to the crisis. Only then will it be possible to repeal or substantially modify this repressive law.

Subscribe to:

Posts (Atom)